Top Advice For Taking Out A Home Mortgage

Content writer-Schneider McDanielHave you ever wanted to buy a home, but you were afraid of a mortgage? Maybe you're worried about taxes and insurance escrow? Perhaps you don't know how to find the right mortgage company and what is a good interest rate? All these questions are going through your mind, and this article is going to help you with a few tips to get you moving in the right direction.

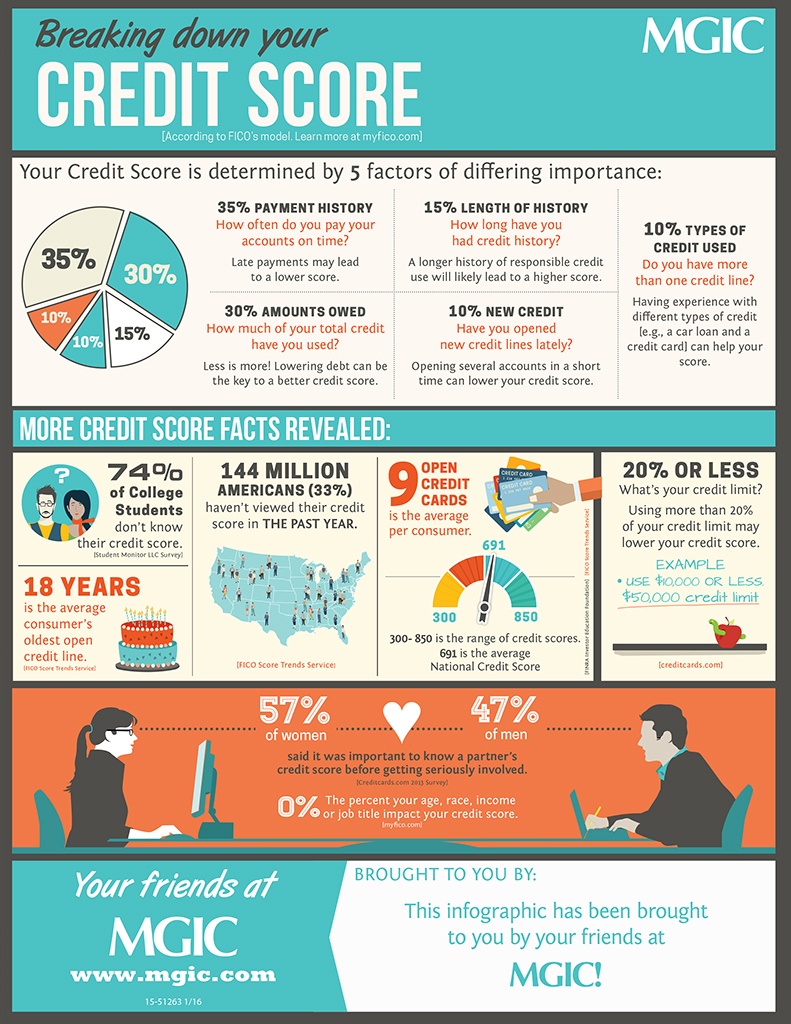

Understand your credit score and how that affects your chances for a mortgage loan. Most lenders require a certain credit level, and if you fall below, you are going to have a tougher time getting a mortgage loan with reasonable rates. A good idea is for you to try to improve your credit before you apply for mortgage loan.

If your mortgage has been approved, avoid any moves that may change your credit rating. Your lender may run a second credit check before the closing and any suspicious activity may affect your interest rate. Don't close credit card accounts or take out any additional loans. Pay every bill on time.

Before getting a mortgage, study your credit history. Good credit is what can help you get a mortgage. Obtain copies of your credit history and scores from the three major credit-reporting bureaus. Study your reports carefully to ensure that no issues or errors must be resolved before you apply. Many lenders need a minimum score of 680, which complies with Freddie Mac and Fannie Mae's guidelines. Most lenders want to avoid scores that are lower than 620.

If your mortgage spans 30 years, think about chipping an additional monthly payment. The extra amount will be put toward the principal amount. This will help you pay your loan even faster and reduce your total interest amount.

Don't make any sudden moves with your credit during your mortgage process. If your mortgage is approved, your credit needs to stay put until closing. After a lender pulls up your credit and says you're approved, that doesn't mean it's a done deal. Many lenders will pull your credit again just before the loan closes. Avoid doing anything that could impact your credit. Don't close accounts or apply for new credit lines. Be sure to pay your bills on time and don't finance new cars.

If you are buying a home for the first time, look into different programs for first time home buyers. Many of these can lower closing costs, find lower-interest mortgage, or lenders that can help you even if you're credit history and score isn't so great.

Find out the property taxes before making an offer on a home. You should understand just how much your property taxes will be before buying a home. You might find the tax assessor values your property higher than you expected and you don't want to have any unpleasant surprises.

Find out if the loan you are applying for is a fixed rate or adjustable rate loan. Generally adjustable rate loans offer lower interest rates; however, the interest rate can increase over time. With an adjustable rate loan, your interest rate can increase yearly; thus costing you more money in the long run.

Know your mortgage interest rate type. When you are obtaining home financing you should understand how the interest is calculated. Your rate could be fixed or it could be adjustable. With fixed interest rates, your payment will usually not change. Adjustable rates vary depending on the flow of the market and are variable.

Never assume that a good faith estimate is fact or written in stone. It is in fact not just an estimate, but one written in good faith. Always be wary of extra costs and fees that can creep into the official and formal paperwork later that drive up your total expense.

Think about your job security before you think about buying a home. If you sign a mortgage contract you are held to those terms, regardless of the changes that may occur when it comes to your job. For example, if you are laid off, you mortgage will not decrease accordingly, so be sure that you are secure where you are first.

Save up as much as you can before you look into buying a home. The more that you have to put down, the better that the terms of your home mortgage contract will be. Essentially, anything that you have to take out on loan could cost you three times that by the end, so save as much as is possible first.

It's easy to stop thinking about maintaining a good financial profile after you've been approved for a loan. Avoid making mistakes during this period that will harm your credit score. Lenders tend to check credit scores even following a loan approval. They can deny the loan at the last minute.

Ask your lender in advance what documentation they need before you meet with them. This is usually going to include tax returns, income statements and W2s, although more might be needed. The more time you have to get it all together is the less likely you'll be unprepared at the actual meeting time.

Make sure that you compare mortgage rates from several companies before you settle on one. Even if the difference seems to be minimal, this can add up over the years. mouse click the next web site can mean thousands of extra you will have to shell out over the course of the loan.

Investigate preapprovals before you start home shopping. Preapproved mortgages will give you an idea of both how much home you can afford plus what your monthly mortgage payments will be. https://www.nav.com/blog/everything-you-need-to-know-about-small-business-banking-1061868/ will set the parameters of your home shopping and save you time not looking at properties you can't realistically afford.

Getting a mortgage without much of a credit history is more difficult and requires you to provide alternative information to get your loan. Keep payment records for up to a year. If you have weak credit, then having proof that you've paid your bills on time will show the lenders your credit worthiness.

During the process of obtaining a mortgage loan, submit any requested documents to your mortgage broker or lender as soon as possible. Taking your time to respond to your lender can delay the date of the closing. Delaying the closing date can put you at risk of losing the rate you have locked-in.

If you know what to look for in a home loan, then you can find the best one for you. This is a commitment which comes with great responsibility, so you do not want to lose control. Rather, you need a mortgage that leaves you breathing room, from a lender you can trust.